Prior to the lockdown, internet banking was on the ascent – however, changes in the manner we live, and work has quickened this cycle as customers of all age segments adopt in- banking app and cashless payments.

The thought that old aged customers can only be served at branches is no more a legitimate thought. Since most customers are currently shying off utilizing ATMs or investing energy at banks. This has made an open door for banks to quicken their digital transformation for customers’ engagement, and to utilize their website and mobile application as a platform for marketing communication.

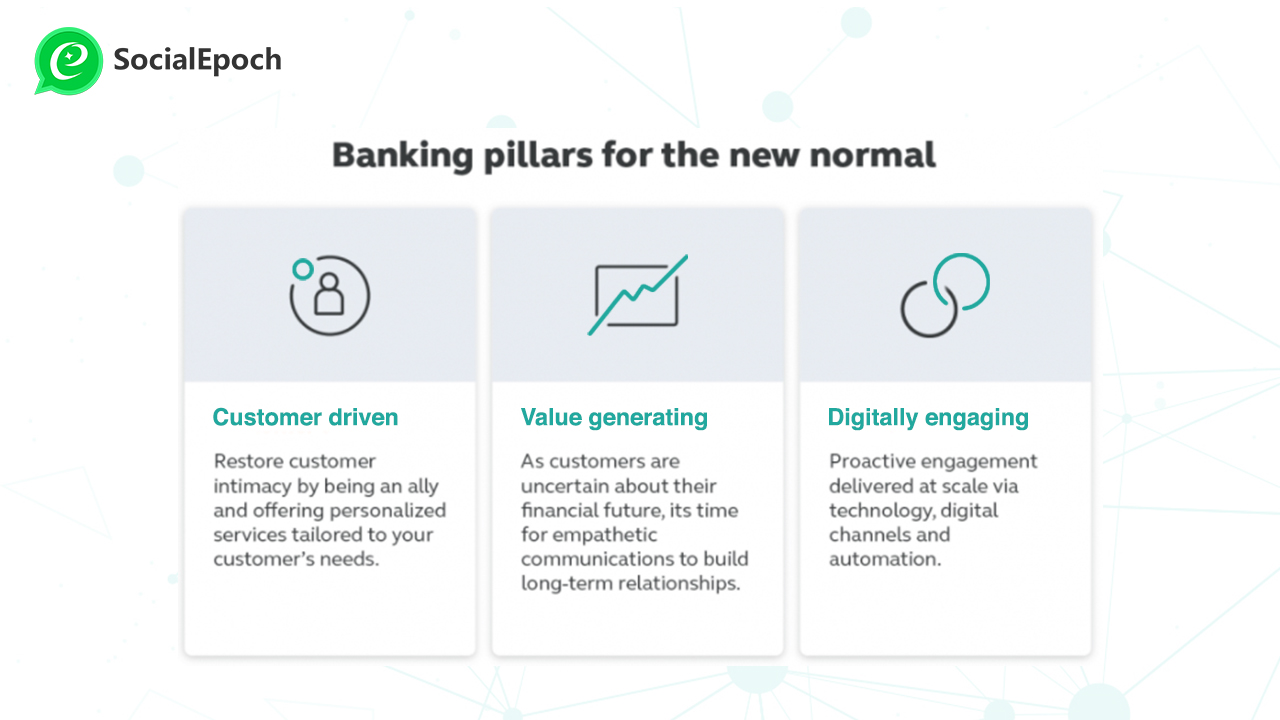

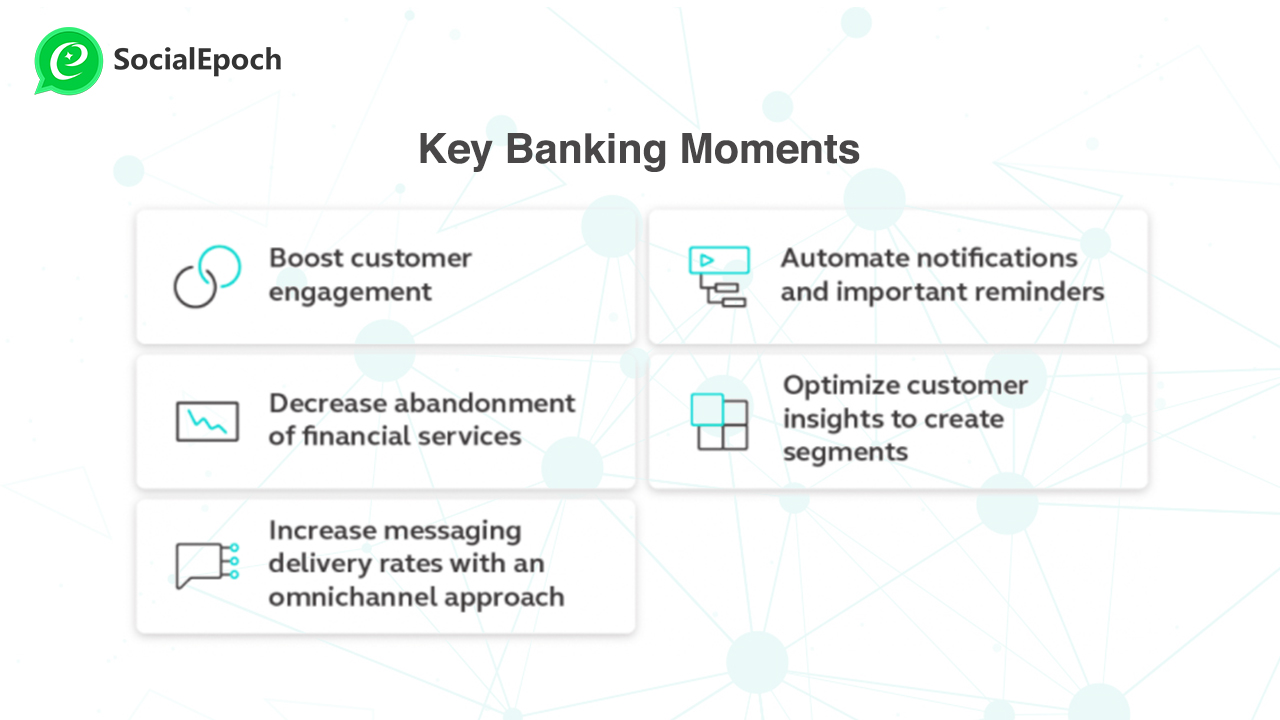

New roadmap for customer engagement

With the future looking questionable, and odds of a subsequent wave, it’s the ideal opportunity for banks to start replanning and designing engagement strategies with customers in such a way that it reflects care for them and support for future financial situation.

- Empower utilization of digital services by customers who have never has used internet banking and draw in them to construct their trust in executing credit only or on the web.

- Show customers that you care for them by proactively using digital channels for communicating with them. For old and vulnerable customers, go the additional mile by informing them about branch timings.

- Analyze and understand customer insights to create pointers for their behavioral triggers, for example, crisis assets for the individuals who over pull back or running low on account balance, and clone crowds to send important messages.

Build relationships based on segmentation

- Re-evaluate your customer segmentation, and embrace communication approach which can help in personalize customer engagement.

- Recognize financial risk factors of customers and offer them short term loan or investment credits.

Segment customer based on transaction activity to offer:

- Credit support

- Proactive credit recommendations and feedback to assist them with making an early move

Add value to drive customer engagement

- Show interest in customers by giving them support for current and future monetary needs, time to time guide them with changes and impacts in products and services offered to them. For example informing customer the way they can manage their money better during the lockdown phase.

- Collect customer insights and pay attention to their needs, feelings, problem. This will help in providing valuable support to them and will boost customer engagement.

The new norm for banking and financial service providers is an adaptation to digital channels with a human touch. It’s very important for all service providers to understand that the time had changed and so customers’ requirements and business cannot just only focus on customer needs but also have to understand their sentiments as well.